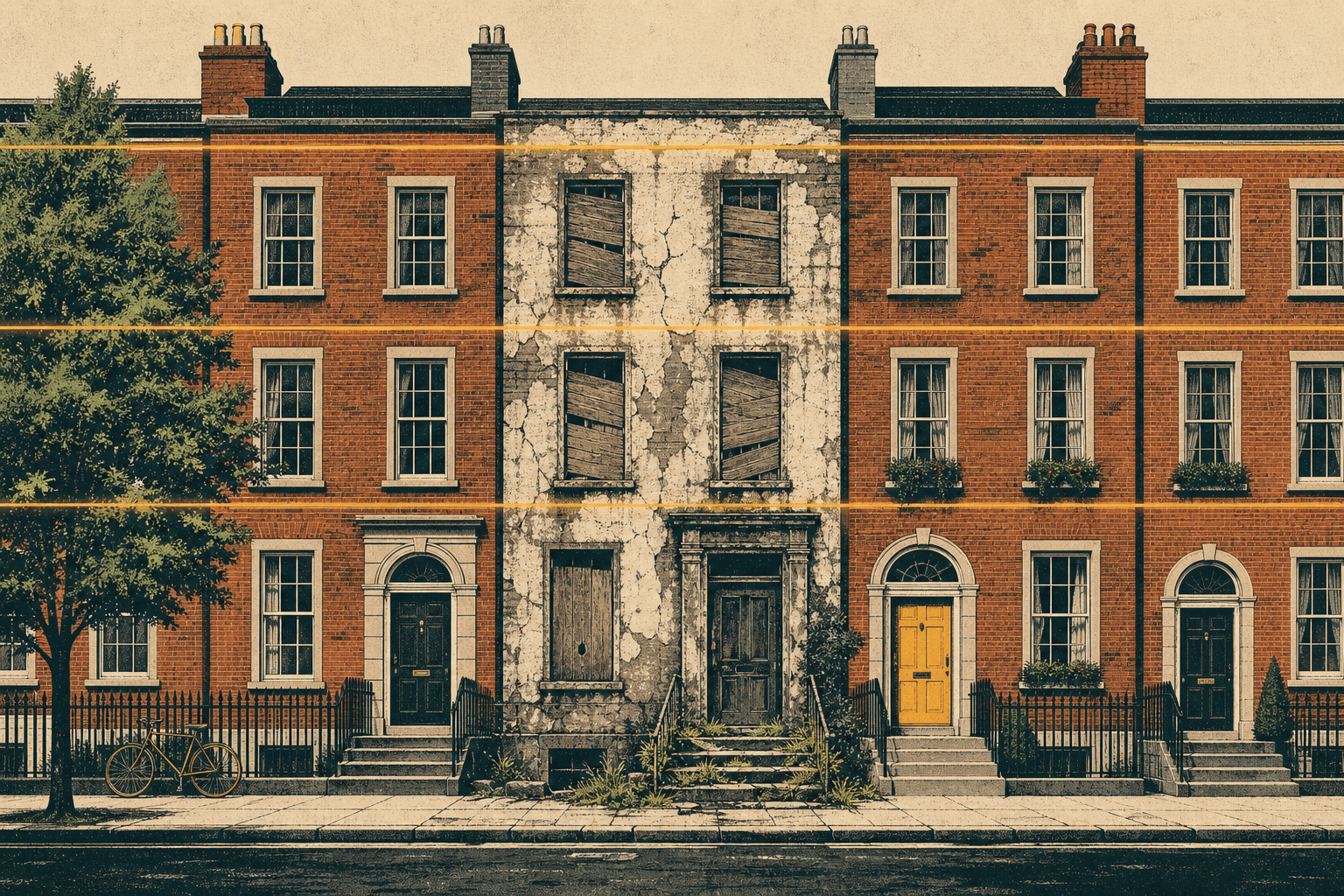

Scattered across Dublin city centre is a blight of derelict buildings. These are an eyesore, a drag on the economy, and by limiting supply they contribute to higher commercial and residential rents. The value these properties is tied to the surrounding neighbourhood. Whose value in turn is dependent on the investment of private individuals and the state through infrastructure etc. Owners watch the value of their property climb from the hard work and effort of others. Benefitting by sitting on property others could put to better, more efficient use, impeding allocative efficiency.

The property rights that allow feckless landowners to leech value from the rest of us are leftovers of feudalism. Landowners have monopoly power as they can refuse to sell except at absurd prices, despite it not being a true reflection of the value.

Land is a gift of nature and belongs to society, not the individual.

Private property and the inequality it creates pose a challenge to prosperity and the political order.

I am not advocating for common ownership, there is some justification for private property. People care best for the things they own, and benefit from any investment made. Common ownership is often afflicted by overuse and neglect, referred to as investment efficiency. Drained aquifers, over-grazed pastures, and neglected staff kitchens are well-known examples.

Impinging on property rights may be anathema to many but the state already encroaches on these rights by using its coercive powers to extract taxes. A quiet, simple way of returning partial ownership of land to society is through taxation on the self-assessed value of the property at which one is required to sell.

Taxation makes it costly to declare a high valuation and thus penalises attempts at exercising monopoly power.

Self-assessment reduces administrative costs and avoids the need for crude valuation systems. An example of self-assessment is claiming races. Owners price their horses before a race and are obliged to sell at this price. The obligation to sell incentivises the owner to price the horse at their true valuation.

By considering the incentives for over and under-valuation we can find the ideal tax rate. Imagine Tom owns a vacant plot which he values at PT. There is some probability (turnover rate), say 30% that someone will come along within a year and wish to purchase the property for more than PT. He might wish to over-value the plot by ΔP in the hopes of gaining on average 30% of ΔP.

If the tax rate is the same as the turnover rate (30%) this gain is offset exactly by the increase in tax (30% of ΔP).

Neither will he want to under-value the plot for fear of selling below his true value. This ensures that every asset passes to the hands of those best able to use it and invest in it, achieving full allocative efficiency.

Many resources already operate in a similar manner. State auctioning of radio spectrum and mineral rights. Web real estate for advertising is distributed using frequent auctions. The constant auctioning of a resource results in it being owned by those who can extract the most value from it.

Hasta la Victoria siempre